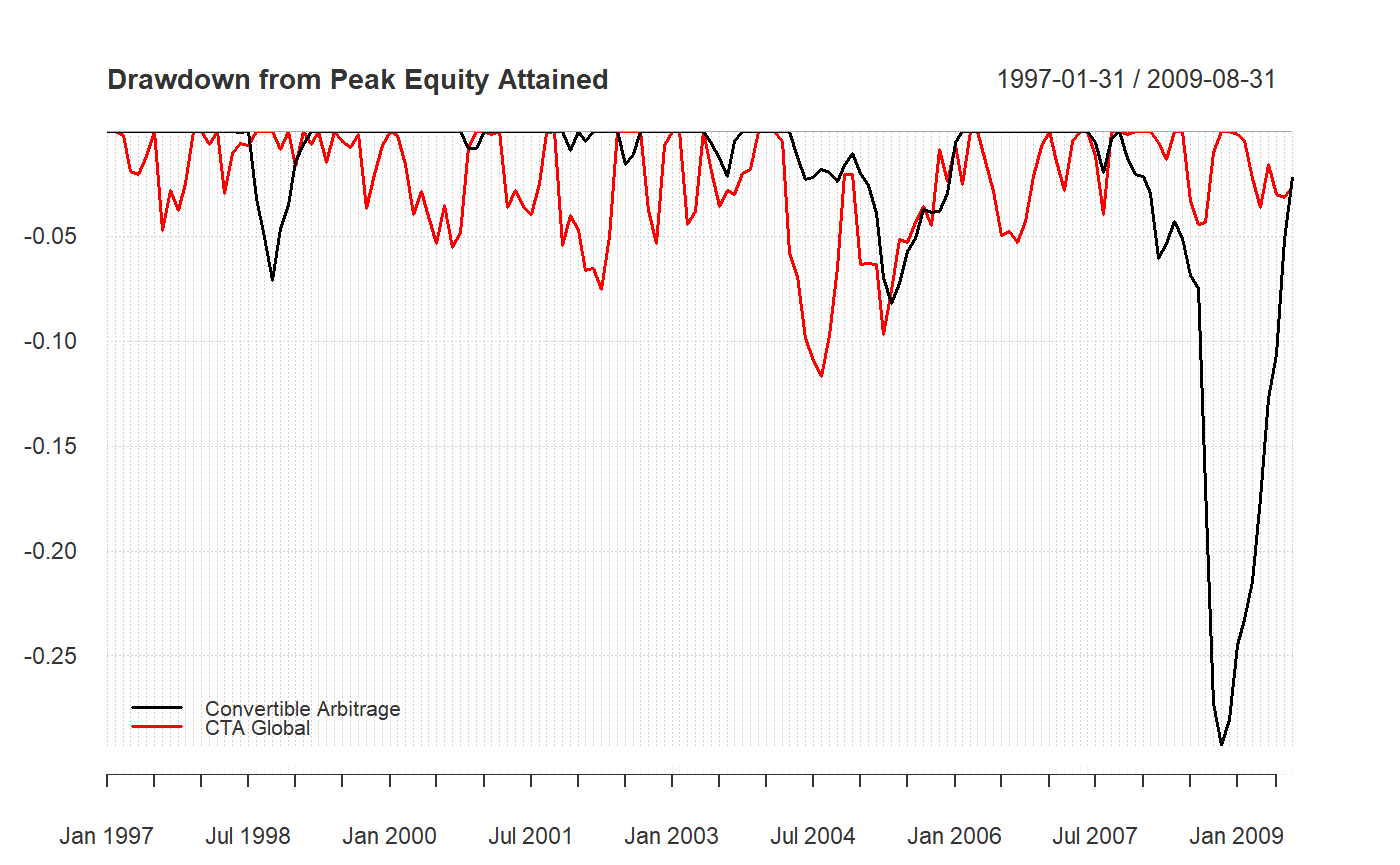

Time series chart of drawdowns through time

A time series chart demonstrating drawdowns from peak equity attained through time, calculated from periodic returns.

chart.Drawdown(R, geometric = TRUE, legend.loc = NULL, colorset = (1:12), ...)

Arguments

| R | an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns |

|---|---|

| geometric | utilize geometric chaining (TRUE) or simple/arithmetic chaining (FALSE) to aggregate returns, default TRUE |

| legend.loc | places a legend into one of nine locations on the chart: bottomright, bottom, bottomleft, left, topleft, top, topright, right, or center. |

| colorset | color palette to use, set by default to rational choices |

| … | any other passthru parameters |

Details

Any time the cumulative returns dips below the maximum cumulative returns, it's a drawdown. Drawdowns are measured as a percentage of that maximum cumulative return, in effect, measured from peak equity.

References

Bacon, C. Practical Portfolio Performance Measurement and Attribution. Wiley. 2004. p. 88

See also

plot

chart.TimeSeries

findDrawdowns

sortDrawdowns

maxDrawdown

table.Drawdowns

table.DownsideRisk

Examples

data(edhec) chart.Drawdown(edhec[,c(1,2)], main="Drawdown from Peak Equity Attained", legend.loc="bottomleft")