Cumulates and graphs a set of periodic returns

Chart that cumulates the periodic returns given and draws a line graph of the results as a "wealth index".

chart.CumReturns(R, wealth.index = FALSE, geometric = TRUE, legend.loc = NULL, colorset = (1:12), begin = c("first", "axis"), ...)

Arguments

| R | an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns |

|---|---|

| wealth.index | if |

| geometric | utilize geometric chaining (TRUE) or simple/arithmetic chaining (FALSE) to aggregate returns, default TRUE |

| legend.loc | places a legend into one of nine locations on the chart: bottomright, bottom, bottomleft, left, topleft, top, topright, right, or center. |

| colorset | color palette to use, set by default to rational choices |

| begin | Align shorter series to:

|

| … | any other passthru parameters |

Details

Cumulates the return series and displays either as a wealth index or as cumulative returns.

References

Bacon, Carl. Practical Portfolio Performance Measurement and Attribution. Wiley. 2004.

See also

chart.TimeSeries plot

Examples

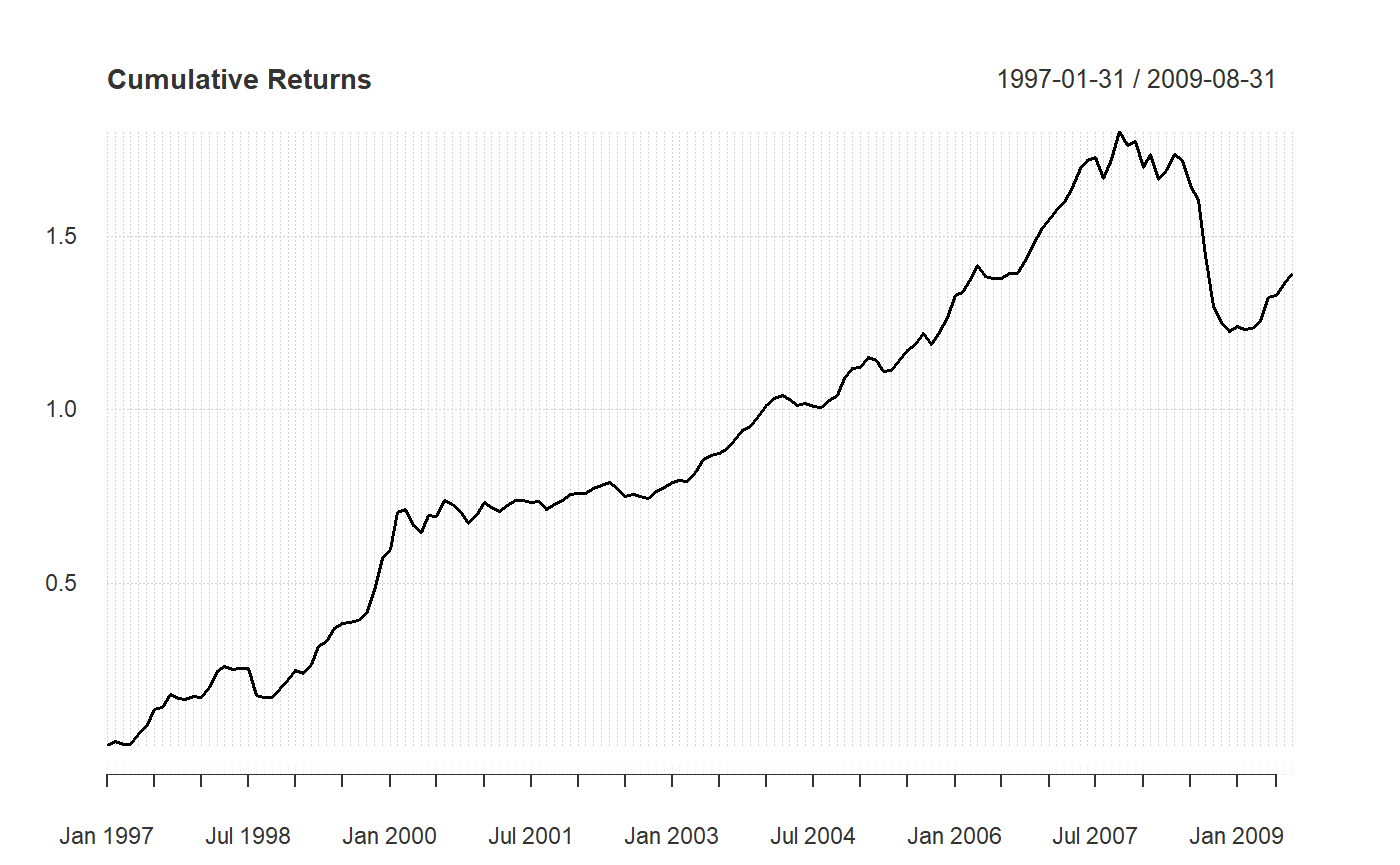

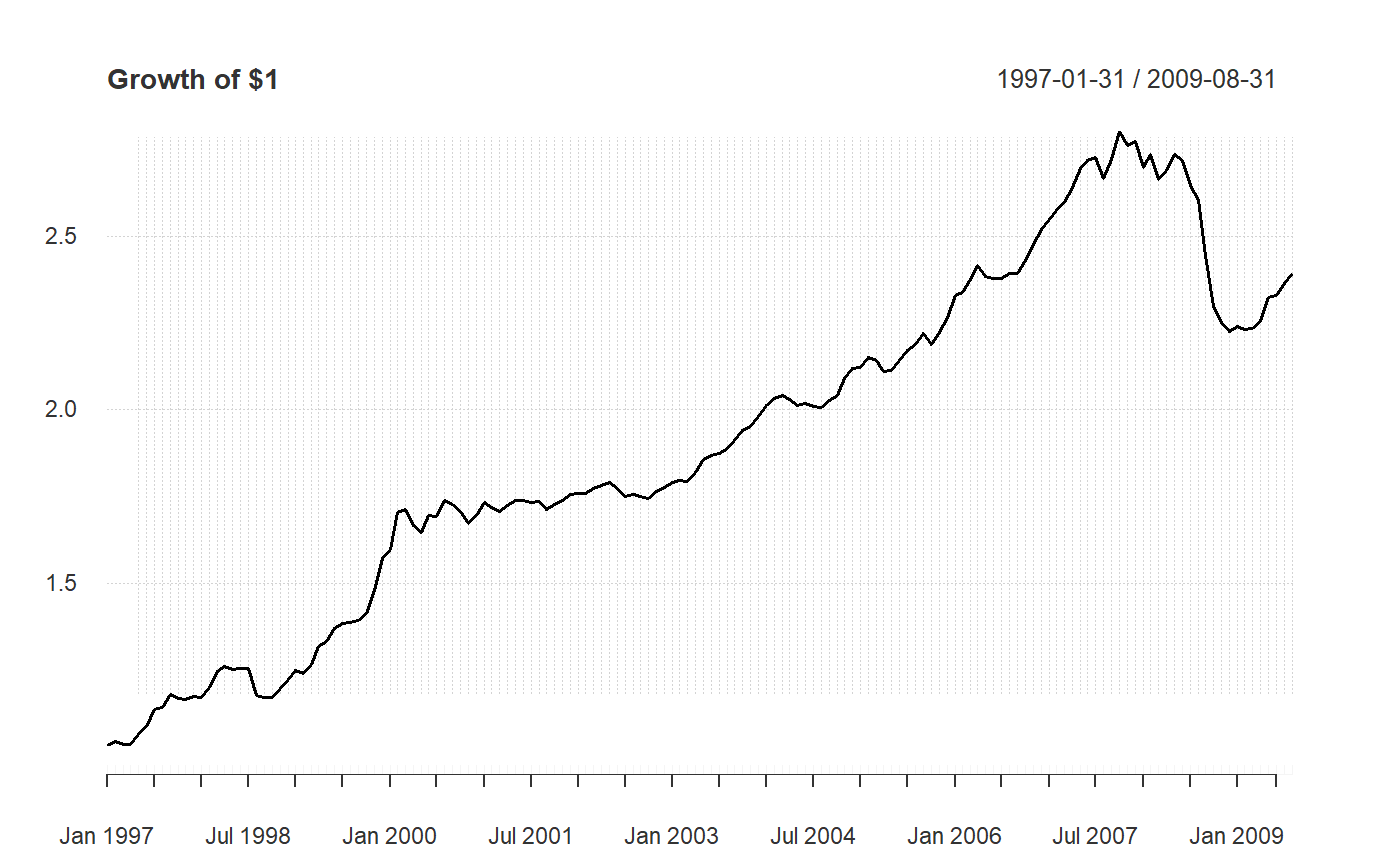

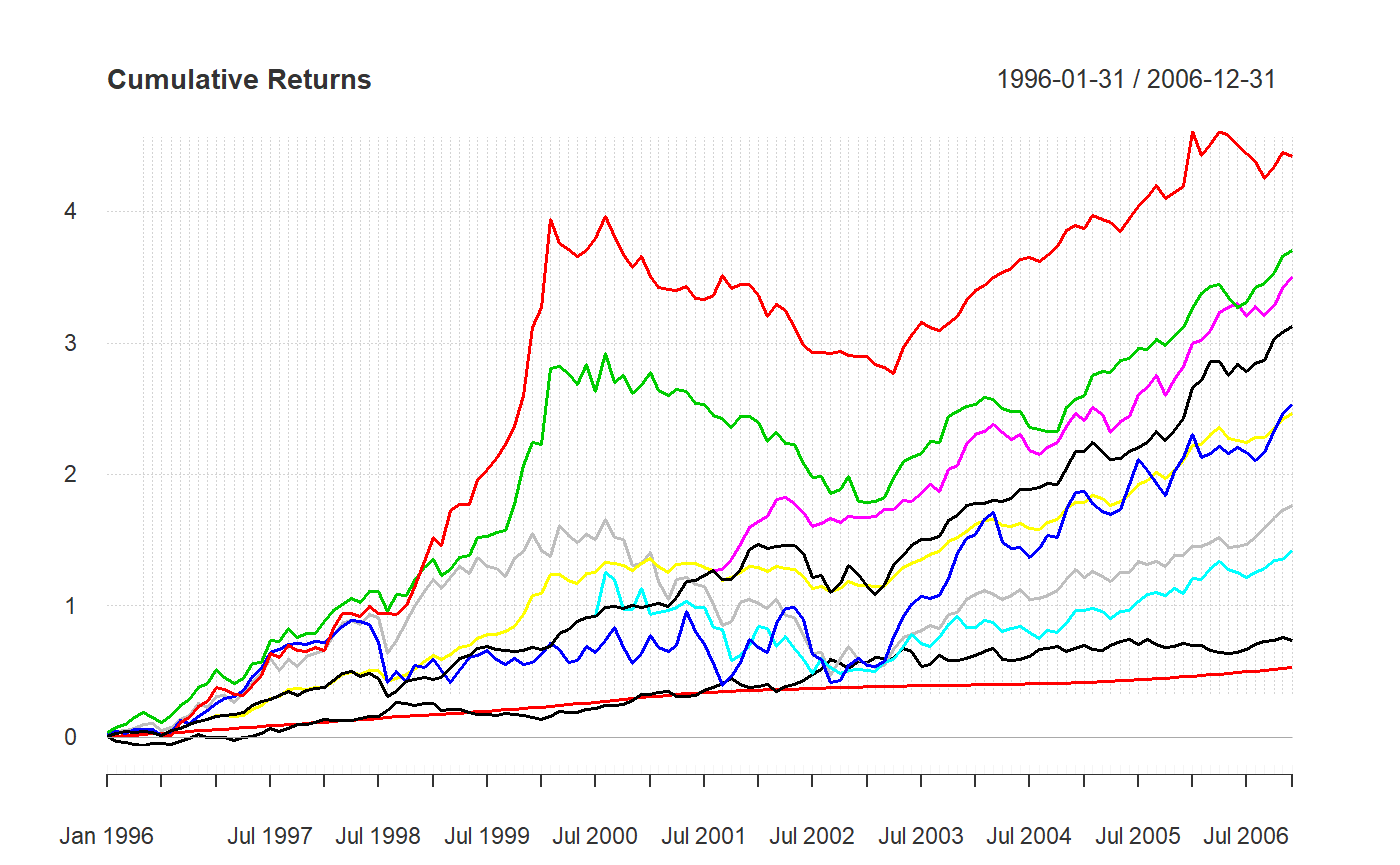

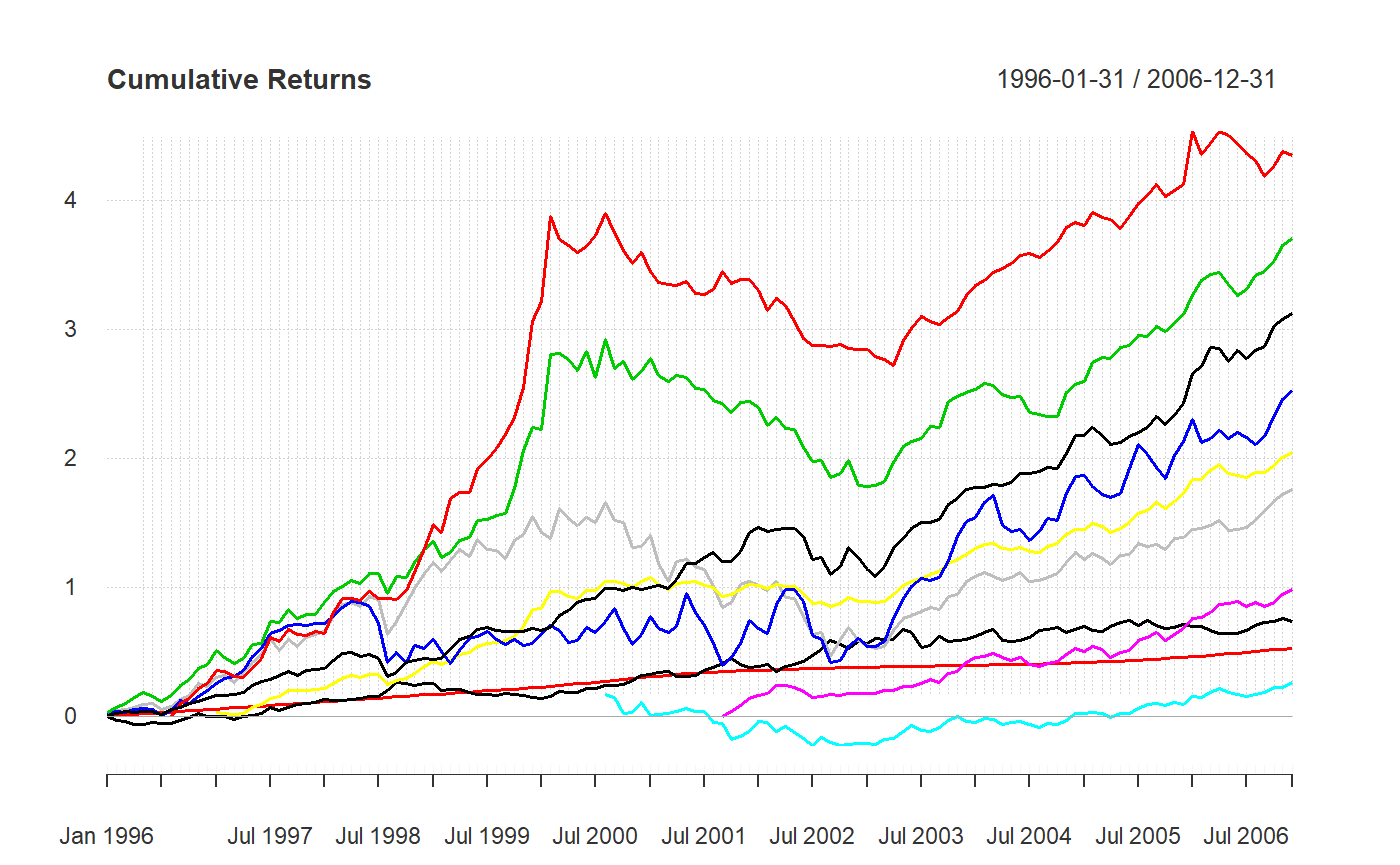

data(edhec) chart.CumReturns(edhec[,"Funds of Funds"],main="Cumulative Returns")chart.CumReturns(edhec[,"Funds of Funds"],wealth.index=TRUE, main="Growth of $1")data(managers) chart.CumReturns(managers,main="Cumulative Returns",begin="first")chart.CumReturns(managers,main="Cumulative Returns",begin="axis")