A wrapper to create charts of relative regression performance through time

A wrapper to create a chart of relative regression performance through time

chart.RollingQuantileRegression(Ra, Rb, width = 12, Rf = 0, attribute = c("Beta", "Alpha", "R-Squared"), main = NULL, na.pad = TRUE, ...) chart.RollingRegression(Ra, Rb, width = 12, Rf = 0, attribute = c("Beta", "Alpha", "R-Squared"), main = NULL, na.pad = TRUE, ...) charts.RollingRegression(Ra, Rb, width = 12, Rf = 0, main = NULL, legend.loc = NULL, event.labels = NULL, ...)

Arguments

| Ra | an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns |

|---|---|

| Rb | return vector of the benchmark asset |

| width | number of periods to apply rolling function window over |

| Rf | risk free rate, in same period as your returns |

| attribute | one of "Beta","Alpha","R-Squared" for which attribute to show |

| main | set the chart title, same as in |

| na.pad | TRUE/FALSE If TRUE it adds any times that would not otherwise have been in the result with a value of NA. If FALSE those times are dropped. |

| … | any other passthru parameters to |

| legend.loc | used to set the position of the legend |

| event.labels | if not null and event.lines is not null, this will apply a list of text labels to the vertical lines drawn |

Details

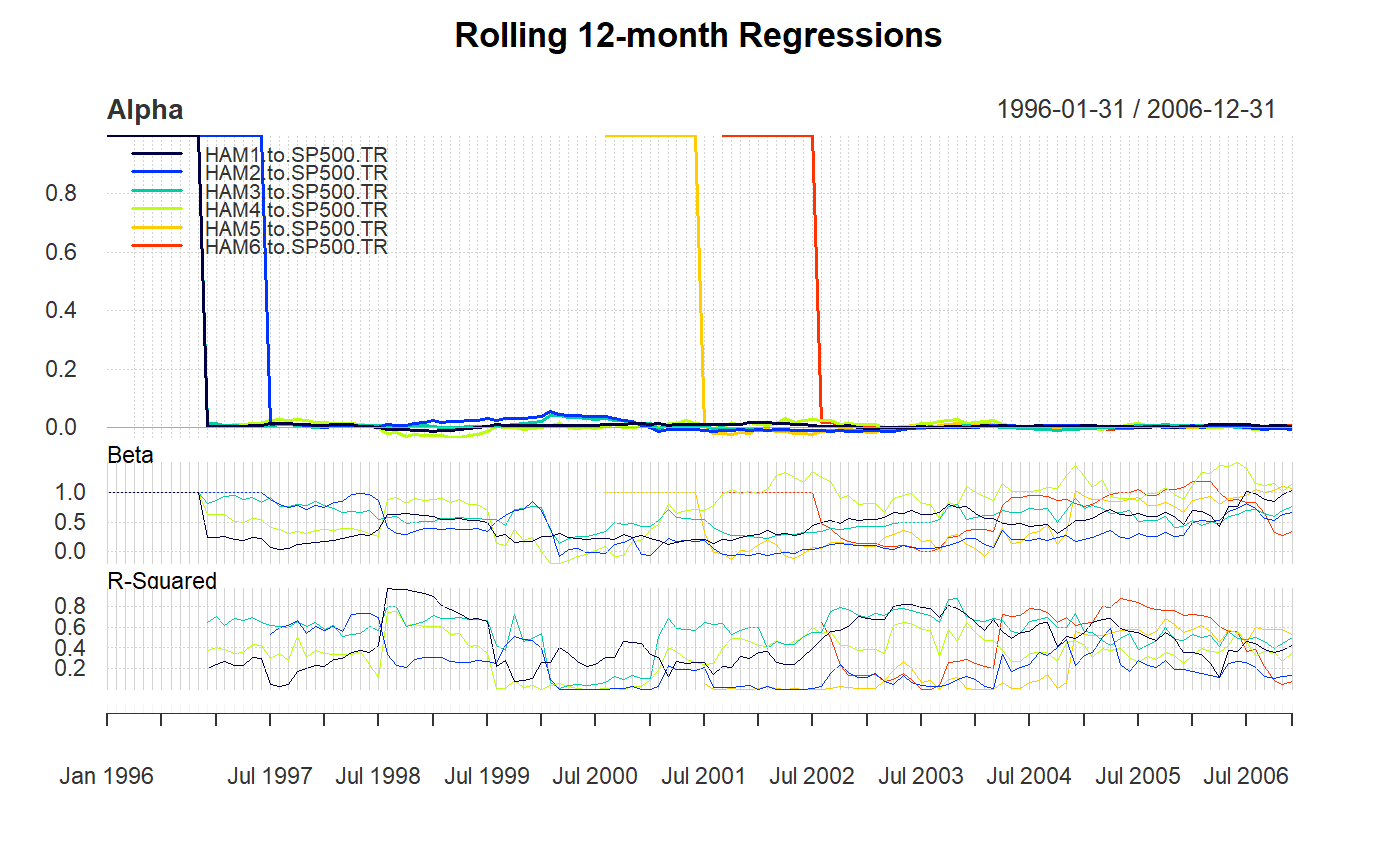

A group of charts in charts.RollingRegression displays alpha, beta,

and R-squared estimates in three aligned charts in a single device.

The attribute parameter is probably the most confusing. In mathematical terms, the different choices yield the following:

Alpha - shows the y-intercept Beta - shows the slope of the regression

line R-Squared - shows the degree of fit of the regression to the data

chart.RollingQuantileRegression uses rq

rather than lm for the regression, and may be more

robust to outliers in the data.

Note

Most inputs are the same as "plot" and are principally

included so that some sensible defaults could be set.

See also

lm rq

Examples

# First we load the data data(managers) chart.RollingRegression(managers[, 1, drop=FALSE], managers[, 8, drop=FALSE], Rf = .04/12)charts.RollingRegression(managers[, 1:6], managers[, 8, drop=FALSE], Rf = .04/12, colorset = rich6equal, legend.loc="topleft")dev.new()#> NULLchart.RollingQuantileRegression(managers[, 1, drop=FALSE], managers[, 8, drop=FALSE], Rf = .04/12)#> Error in chart.RollingQuantileRegression(managers[, 1, drop = FALSE], managers[, 8, drop = FALSE], Rf = 0.04/12): package‘quantreg’is needed. Stopping# not implemented yet #charts.RollingQuantileRegression(managers[, 1:6], # managers[, 8, drop=FALSE], Rf = .04/12, # colorset = rich6equal, legend.loc="topleft")